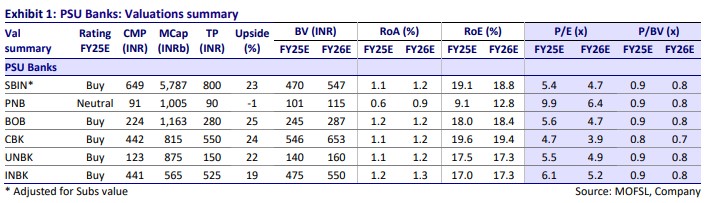

Earnings outlook steady; well poised for Re-rating 2.0 PSBs have delivered a strong performance since FY22, with the Nifty PSU Bank Index outperforming the Nifty-50/Bank Nifty by 87%/ 78%. We earlier resumed coverage on the entire PSB sector in CY21 enthused by their improving business/earnings outlook. We estimate top six PSBs under our coverage to report PAT of INR1.5t/INR1.7tn in FY25/FY26, while sector RoA/RoE improves to 1.2%/17.9% by FY26E. Several PSBs have raised capital from the market and have shored up their capitalization levels, which will enable healthy balance sheet growth, particularly as the capex cycle recovers after the general elections. We thus estimate ABV for our coverage PSBs to grow at a healthy 16-22% range over FY24-26. We believe that sustained and consistent performance on return ratios and a conducive macroenvironment can drive further re-rating of the sector. We introduce FY26E and rollforward target prices for our PSBs coverage universe. We thus revise our TP for SBI (INR800), BoB (INR280), INBK (INR525), UNBK (INR150), CBK (INR550), PNB (INR90). Top picks: SBIN, BOB and CBK.

Download Pdf of research report on Best PSU Banks stocks to buy: Click here to Download

Image uploaded by Shyam Sundar :